The Autorité des Marchés Financiers (AMF) notes that the new reference rates are still being neglected by professionals, despite the disappearance of the old IBOR rates at the end of the year. The stakes are high, however, especially for derivatives.

The transition to the new benchmark rates remains an element of short-term risk, the AMF (Autorité des Marchés Financiers) said yesterday in its mapping 2021.

The market watchdog notes that financial players are not sufficiently prepared for this major reform, which will see the old benchmark rates disappear by the end of 2021 for most of them. These are the famous IBORs (Libor, Euribor, etc.) for Interbank Offered Rates, well known to financial market professionals.

"IBOR rates, like Libor (London interbank offered rate), or Euribor (Euro interbank offered rate) are among the rates that have played a key role in financing the economy and markets in recent decades. Contracts and financial products linked to IBORs have reached hundreds of billions of dollars"Société Générale reminds us on its website.

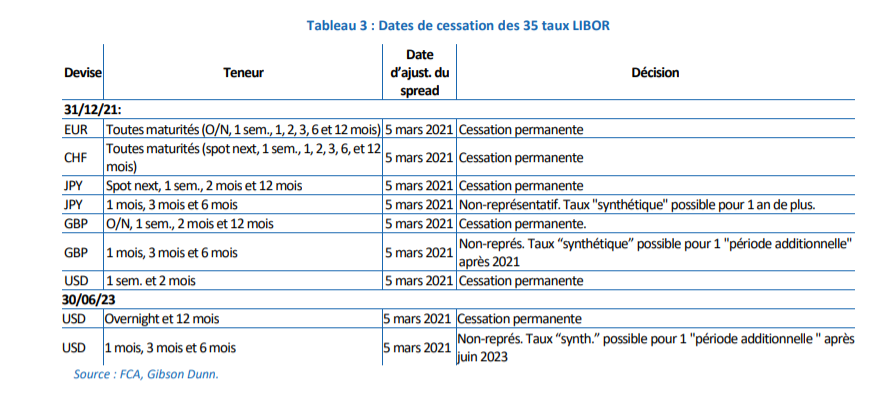

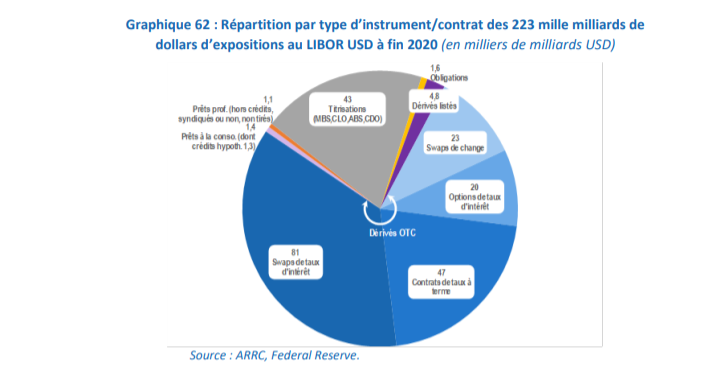

More than 400,000 billion dollars of notional amounts of derivatives, credits and other financial products are referenced to IBOR. LIBORs alone account for some 230,000 billion in notional amounts, including 76.7% in OTC derivatives, the AMF said.

But these "predetermined" rates, based on the declarations of the contributing banks, showed their limits and their lack of reliability during the 2007-2008 crisis.

"Since 2014, central bank-led working groups have chosen Risk Free Rates (RFRs) as alternatives to IBORs. RFRs are "post-determined" rates constructed on the basis of transactions carried out on deposits with banks on a day-to-day basis"Société Générale continues.

These changes have been incorporated into the EU Benchmark Regulation which came into force in 2018.

Today, the regulator nevertheless highlights the efforts and substantial progress already made: "Transition plans are being deployed by the major banks and market infrastructures (e.g. clearing houses), which are substituting RFRs for existing rates and adopting contractual fallback clauses to manage the cessation of the calculation of rates in use. With the support of the authorities, the financial industry is devoting significant resources to systematising the identification of exposures to IBORs, implementing transition processes and developing appropriate systems".

Gaps to be filled

The AMF also notes numerous examples of already effective use of RFRs, such as for the issuance of bonds indexed to the SOFR (Secured Overnight Financing Rate) and SONIA (Sterling Over Night Index Average, (SONIA) in autumn 2018 under the aegis of the World Bank, or the use of the €STR (euro area interbank reference rate) in February 2021 to calculate the Livret A rate in France.

But there are still important gaps to be filled: "In particular, the processing of certain types of contracts (e.g. syndicated loans) cannot be automated, and certain types of players (e.g. non-financial companies) have been slow to adopt them. Even in the most advanced futures markets, the adoption of RFRs is still limited. In this context, a major issue concerns dollar LIBORs, for which the deadline for transition has been extended to June 2023".