Eurozone government bonds are incorporating the firmness of the ECB, which is initiating a rate hike cycle and putting an end to its asset purchases. But the central bank must take into account the risk of a bond market dislocation, of which Italy would be the first victim. Christine Lagarde says she is ready to deploy an "anti-fragmentation" instrument if necessary.

This is a bond correction of historic proportions. With the ECB's monetary policy committee on Thursday, the fall in government bonds accelerated further. The yield on the French 10-year OAT reached 2%, double the March level. The benchmark bond was still showing a negative rate at the end of last year.

Forced to act to limit strong inflationary pressures in the eurozone (8.1% in May year-on-year), the European Central Bank announced a 25 basis point rate hike on July 21, the first since 2011. It is also planning another hike in September, perhaps on a larger scale (50 basis points) if the price situation so requires.

Currently set at -0.5 % and negative for the past 8 years, the ECB deposit rate could thus return to positive territory by the end of the third quarter. Going forward, "we expect the ECB to return to normal interest rate actions at the October and December meetings and not to raise interest rates by more than 125 basis points in total this year"Reto Cueni, chief economist at Vontobel AM, anticipates.

End of asset purchases

At the same time, the central bank ended its asset purchases under the Asset Purchasing Program (APP) at the beginning of July.

"The APP, which includes purchases of asset-backed securities, covered bonds, corporate bonds and government bonds, totaled just under 3.25 trillion euros last month. This is the first and largest quantitative easing (QE) program, originally introduced to combat deflationary pressures. The second program, introduced to deal with the pandemic (Emergency Pandemic Purchase Program, or EPPP), was completed in March, with 1.7 trillion euros of government bonds"Azad Zangana, senior economist for Europe at Schroders, said.

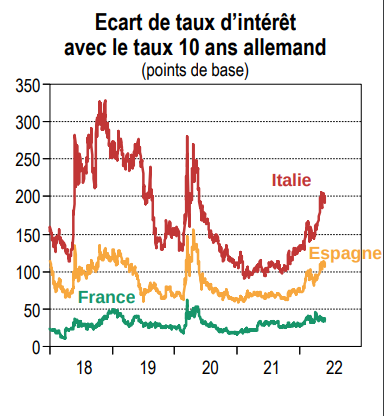

Sovereign debt crisis

However, the withdrawal of this support, coupled with the rate hikes, poses a risk to growth and the bond market in a context where governments and companies are faced with their debt burden and a gradual increase in their interest charges. The spread between German and Italian government bonds continues to widen, to around 215 basis points. The Italian 10-year sovereign rate reached 3.7 % on Thursday, up from 0.55% a year ago.

To avoid the risk of market dislocation in the Eurozone and a new sovereign debt crisis, the ECB has been hinting at intervention for several weeks. "If necessary, as we have amply demonstrated in the past, we will deploy either adjusted existing instruments or new instruments that will be made available"This was confirmed by Christine Lagarde, the president of the central bank, at the press conference following the meeting of the Board of Governors.

"We are determined, determined, to ensure adequate transmission of monetary policy and thus to avoid fragmentation to the extent that it would weaken that transmission."However, she did not elaborate.

New purchasing program?

According to Florence Pisani, head of economic research at Candriam, the ECB needs an anti-fragmentation tool to avoid an uncontrolled spread widening, which would take the form of a new asset purchase program to be triggered if the situation requires it. Nevertheless, it believes that the markets will test the central bank's resolve to activate such a device.

Anna Stupnytska, Global Economist at Fidelity International, has reservations about this possibility: "While a new spread management tool may help prevent fragmentation, it will not be a silver bullet, as it will likely lead to a new set of problems for the ECB, including moral hazard".

In other words, governments would once again be tempted to let their budget deficits slip, relying on central bank support as a last resort.

France, whose debt has increased significantly in recent years, seems to be spared by investors for the time being, as evidenced by the relative stability of the spread with Germany, at around 50 basis points. For Philippe Gudin, senior economist at Barclays Europe, "the situation in France, which enjoys a much better economic performance and credibility, is not comparable to that of Italy". The expert rules out any problem with debt sustainability on this side of the Alps.

Additional cost

In a speech given a month ago at the conference of the High Council of Public Finance, the Governor of the Banque de France expressed his concern: " According to our estimates, each 1% increase in rates will lead to an increase in the annual interest burden of 1 point of GDP after 10 years, and an increase in the debt of 5½ points of GDP, compared to a situation without rate increases. Each 1% increase in interest rates therefore represents an additional annual cost of nearly €40 billion, or almost the current defense budget".

For François Villeroy de Galhau, the rate of increase in spending must be reduced, at least for the sake of solidarity with future generations and with the objective of reducing the debt "within 10 years well below 100 % of GDP", compared to about 113 % today.

The 2022 Finance Law expected the 10-year OAT rate to be 0.75 % at the end of the year.