The amount of French issues now exceeds that of German Pfandbriefs, according to S&P. This trend is attributed by the law firm Gide to a very dynamic real estate credit market and a balanced and appropriate regulatory framework.

French covered bonds have done very well. According to S&P, issuance amounts exceeded those of German Pfandbriefs for the first time in 2020, at €27.4bn, compared with €26bn a year earlier. Due to the health crisis, the overall volume of issuance across all countries at the same time contracted by 30 % compared to 2019. France now accounts for almost a third (31%) of the total market.

9.8 billion of issuance since the beginning of the year in France, or 30.5 % of the total.

19 broadcast programs

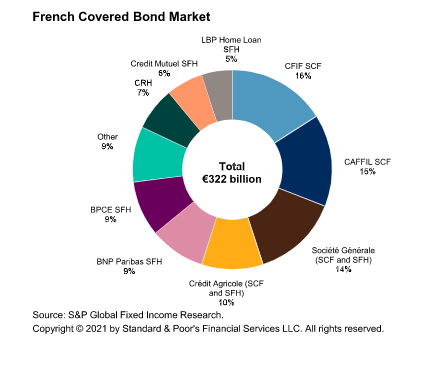

France's covered bonds outstanding are the second largest in the world, at EUR 321.6 billion. In France, there are a total of 19 issue programmes from 14 banks and one company, the rating agency points out.

Perceived as a very low-risk asset class, these bonds are backed by a pool of underlying assets: mortgages, housing loans and, to a lesser extent, public sector loans. They are liquid and offer investors a higher return than government bonds.

"The rise of French covered bonds is due to the fact that issuers continue to rely on issues placed with investors, whereas most other European banks have turned to other sources, such as central bank refinancing operations"This is a good thing," says Adriano Rossi, a credit analyst at S&P.

Difference from German Pfandbriefs

For his part, Xavier de Kergommeaux, a partner at Gide, Loyrette, Nouel, puts this trend down to an extremely dynamic mortgage market in France and a balanced and appropriate regulatory framework:

"The fundamental difference between Pfandbriefs and French covered bonds is that the latter are issued by specialised subsidiaries. Unlike in Germany, there is a very clear separation between the entity that originates the loans and the entity that issues the securities and to which the receivables have been assigned in a rational approach.".

Two distinct legal frameworks

French covered bond legislation encompasses two distinct legal frameworks: the société de crédit foncier (SCF), which dates back to 1999, and the société de financement de l'habitat (SFH), which was created in 2010 to adapt to the specificities of the housing market. The latter restricts the guarantees eligible for residential loans.

"The status of SFH was created because the bulk of French banks' outstanding home loans are non-mortgage loans and are based on home loan guarantees. However, SCFs can only hold guaranteed loans up to a limit of 35% of their assets"says Xavier de Kergommeaux. These "housing bonds" have become a privileged source of financing for credit institutions such as Société Générale, BNP Paribas and Crédit Agricole.

According to Adriano Rossi, the French regulatory framework is already well aligned with the European texts, the directive currently being transposed and the regulation, which aim to harmonise covered bond market practices on the continent: "We understand that the legislative amendments (...) are expected to be approved by the French Parliament in time for the 8 July 2021 harmonisation directive deadline. We also understand that the regulatory aspects will be implemented later, for the 8 July 2022 deadline".

Green covered bonds

For the full year 2021, the rating agency nevertheless expects issuance amounts to be lower than in 2020, due to issuers' access to cheap central bank funding as well as very abundant bank deposits.

It should also be noted, as S&P points out, that France is the leader in the field of green covered bonds, i.e. those dedicated to financing impact projects:

"Green and social covered bonds remain a priority for French issuers since 2020. This year we have seen significant issuance, including Caisse Française de Financement Local's (Caffil) €750 million social bond in April. BPCE issued €1.25bn of SFH green bonds in May 2020 and another €1.5bn in May 2021. We expect other French entities to become sustainable covered bond issuers by the end of the year and early 2022"Adriano Rossi believes.